![]()

![]()

Backtest trading strategies with Python.

Kudos to Zach Lûster for the original project kernc/backtesting.py

which he built and maintained for 5 years.

We at LUCIT like to use backtesting.py with our customers in smaller projects.

Unfortunately the project is missing important updates, and therefore we decided to fork the project and release new

stable versions.

We are happy to maintain our forked repository and take care of code reviews, pull requests and releases and hope for good support from the community!

The package lucit-backtesting is a Python framework for inferring viability of trading strategies on historical (past)

data. Of course, past performance is not indicative of future results, but a strategy that proves itself resilient in a

multitude of market conditions can, with a little luck, remain just as reliable in the future. Improved upon the vision

of Backtrader, and by all means surpassingly comparable to other accessible alternatives, Backtesting.py is lightweight,

fast, user-friendly, intuitive, interactive, intelligent and, hopefully, future-proof. It is also documented well,

including a handful of tutorials.

| Feature | Description |

|---|---|

| Compatible with forex, crypto, stocks, futures ... | Backtest any financial instrument for which you have access to historical candlestick data. |

| Blazing fast, convenient | Built on top of cutting-edge ecosystem libraries (i.e. Pandas, NumPy, Bokeh) for maximum usability. |

| Small, clean API | The API reference is easy to wrap your head around and fits on a single page. |

| Technical indicator library agnostic | Compatible with any sensible technical analysis library, such as TA-Lib or Tulip. |

| Built-in optimizer | Test hundreds of strategy variants in mere seconds, resulting in heatmaps you can interpret at a glance. |

| High-level API | Think market timing, swing trading, money management, stop-loss and take-profit prices, leverage, machine learning ... |

| Interactive visualization | Simulated trading results in telling interactive charts you can zoom into. See Example. |

| Vectorized or event-based backtesting | Signal-driven or streaming, model your strategy enjoying the flexibility of both approaches. |

| Composable strategies | Contains a library of predefined utilities and general-purpose strategies that are made to stack. |

You can have either backtesting.py or lucit-backtesting installed, but not both!

$ pip uninstall backtesting

$ pip install lucit-backtesting

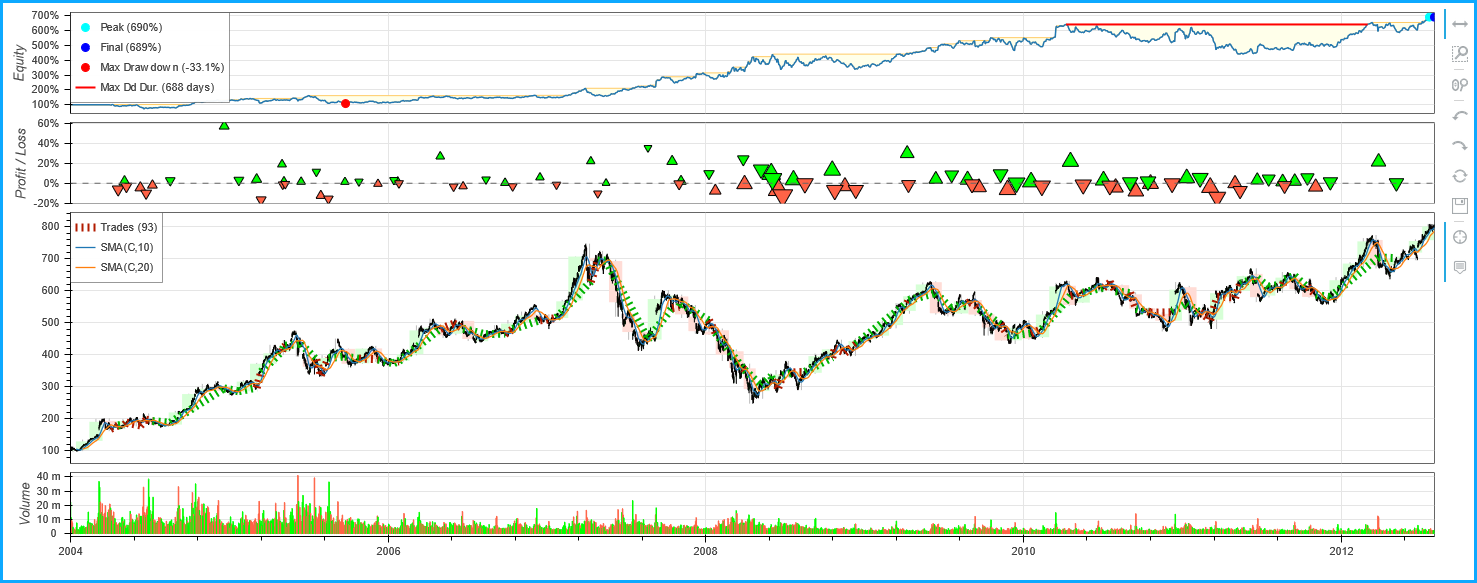

The example shows a simple, unoptimized moving average cross-over strategy. It's a common introductory strategy and a pretty decent strategy overall, provided the market isn't whipsawing sideways.

We begin with 10,000 units of currency in cash, realistic 0.2% broker commission, and we trade through 9 years worth of Alphabet Inc. stock.

Whenever the fast, 10-period simple moving average of closing prices crosses above the slower, 20-period moving average, we go long, buying as many stocks as we can afford. When it crosses below, we close our long position and go short (assuming the underlying instrument is actually a CFD and can be shorted).

We record most significant statistics this simple system produces on our data, and we show a plot for further manual inspection.

from backtesting import Backtest, Strategy

from backtesting.lib import crossover

from backtesting.test import SMA, GOOG

class SmaCross(Strategy):

def init(self):

price = self.data.Close

self.ma1 = self.I(SMA, price, 10)

self.ma2 = self.I(SMA, price, 20)

def next(self):

if crossover(self.ma1, self.ma2):

self.buy()

elif crossover(self.ma2, self.ma1):

self.sell()

bt = Backtest(GOOG, SmaCross, commission=0.002, exclusive_orders=True)

stats = bt.run()

bt.plot()

print(f"\r\nOverview:\r\n{stats}\r\n")

print(f"\r\nEquity:\r\n{stats['_equity_curve']}\r\n")

print(f"\r\nTrades:\r\n{stats['_trades']}")

Results in:

Overview:

Start 2004-08-19 00:00:00

End 2013-03-01 00:00:00

Duration 3116 days 00:00:00

Exposure Time [%] 94.27

Equity Final [$] 68935.12

Equity Peak [$] 68991.22

Return [%] 589.35

Buy & Hold Return [%] 703.46

Return (Ann.) [%] 25.42

Volatility (Ann.) [%] 38.43

Sharpe Ratio 0.66

Sortino Ratio 1.30

Calmar Ratio 0.77

Max. Drawdown [%] -33.08

Avg. Drawdown [%] -5.58

Max. Drawdown Duration 688 days 00:00:00

Avg. Drawdown Duration 41 days 00:00:00

# Trades 93

Win Rate [%] 53.76

Best Trade [%] 57.12

Worst Trade [%] -16.63

Avg. Trade [%] 1.96

Max. Trade Duration 121 days 00:00:00

Avg. Trade Duration 32 days 00:00:00

Profit Factor 2.13

Expectancy [%] 6.91

SQN 1.78

Kelly Criterion 0.6134

_strategy SmaCross(n1=10, n2=20)

_equity_curve Equ...

_trades Size EntryB...

dtype: object

Equity:

Equity DrawdownPct DrawdownDuration

Date

2023-01-02 13:03:00 10000.00000 0.000000 NaT

2023-01-02 13:04:00 10000.00000 0.000000 NaT

2023-01-02 13:05:00 10000.00000 0.000000 NaT

2023-01-02 13:06:00 10000.00000 0.000000 NaT

2023-01-02 13:07:00 10000.00000 0.000000 NaT

... ... ... ...

2024-01-01 00:55:00 11585.32229 0.050322 NaT

2024-01-01 00:56:00 11585.32229 0.050322 NaT

2024-01-01 00:57:00 11585.32229 0.050322 NaT

2024-01-01 00:58:00 11585.32229 0.050322 NaT

2024-01-01 00:59:00 11585.32229 0.050322 51 days 18:57:00

Trades:

Size EntryBar ExitBar EntryPrice ExitPrice PnL ReturnPct EntryTime ExitTime Tag Duration

0 6 23305 23305 1524.62018 1517.480252 -42.839567 -0.004683 2023-01-18 17:28:00 2023-01-18 17:28:00 None 0 days 00:00:00

1 6 23308 23568 1522.60415 1521.180000 -8.544900 -0.000935 2023-01-18 17:31:00 2023-01-18 21:51:00 None 0 days 04:20:00

2 6 23569 32957 1525.95417 1543.780000 106.954980 0.011682 2023-01-18 21:52:00 2023-01-25 10:20:00 None 6 days 12:28:00

3 6 32958 40820 1546.69621 1542.810000 -23.317260 -0.002513 2023-01-25 10:21:00 2023-01-30 21:23:00 None 5 days 11:02:00

4 6 40821 43959 1550.01614 1690.310000 841.763160 0.090511 2023-01-30 21:24:00 2023-02-02 01:42:00 None 2 days 04:18:00

.. ... ... ... ... ... ... ... ... ... ... ...

78 5 488520 488665 2205.67724 2184.630000 -105.236200 -0.009542 2023-12-11 19:03:00 2023-12-11 21:28:00 None 0 days 02:25:00

79 5 488666 488673 2192.94917 2185.350000 -37.995850 -0.003465 2023-12-11 21:29:00 2023-12-11 21:36:00 None 0 days 00:07:00

80 5 488674 489911 2191.03344 2187.110000 -19.617200 -0.001791 2023-12-11 21:37:00 2023-12-12 18:14:00 None 0 days 20:37:00

81 5 489912 503782 2188.65633 2305.250000 582.968350 0.053272 2023-12-12 18:15:00 2023-12-22 09:25:00 None 9 days 15:10:00

82 5 514701 517609 2277.31150 2259.124026 -90.937372 -0.007986 2023-12-29 23:24:00 2023-12-31 23:52:00 None 2 days 00:28:00

Before reporting bugs or posting to the discussion board and please read contributing guidelines. We thank you!

Do you need a developer, operator or consultant? Contact us for a non-binding initial consultation!